Veja também

21.01.2026 09:14 AM

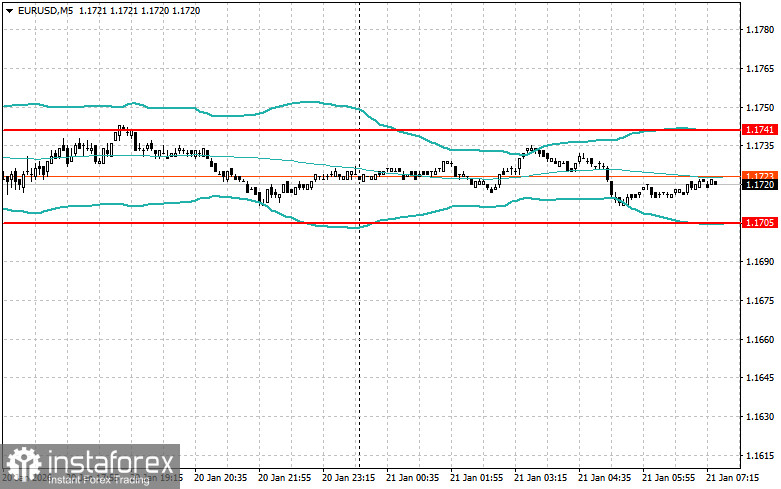

21.01.2026 09:14 AMThe dollar continued its active decline against risk assets. It suffered the most versus the euro, which traders actively bought for several reasons.

The risk that European countries holding trillions of dollars in US bonds and equities could start selling them triggered yesterday's strong rally in the euro. Market participants, worried about the prospect of a transatlantic trade war, do not currently view the dollar as a safe-haven asset. Although such a scenario is unlikely, even given Trump's aggressive rhetoric and protectionist measures, one must be prepared for anything. European leaders could decide to take retaliatory measures against Trump's tariffs using financial levers. Selling US assets held by European central banks and sovereign funds could significantly weaken the dollar and destabilise the US financial system.

There is no eurozone data scheduled for the first half of today; only speeches by European Central Bank President Christine Lagarde and Bundesbank President Joachim Nagel are expected. Most likely, the policymakers will comment on Greenland and on measures they might take if Trump unleashes another trade war.

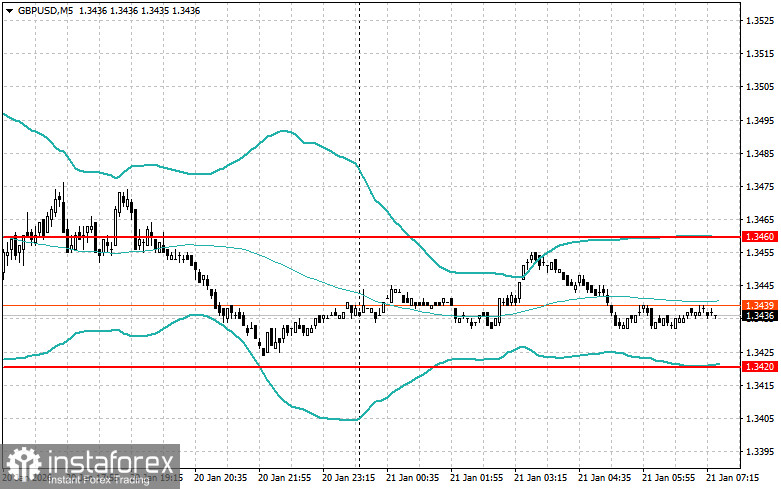

As for the pound, in the first half of the day, UK CPI, core CPI, and input/output price indices are due. These releases will certainly affect sterling, but their effect will probably be short-lived and limited, given the market's predominant focus on the Greenland issue. If inflation readings beat expectations, the pound may get a short-term boost, as this would strengthen arguments for a tighter Bank of England policy. However, against the backdrop of overall uncertainty and heightened geopolitical risk related to Greenland, investors are unlikely to make long-term decisions based solely on UK data.

If the data match economists' expectations, prefer a Mean Reversion strategy. If the data are much higher or lower than economists' expectations, it is best to use a Momentum strategy.