Lihat juga

30.06.2026 06:43 PM

30.06.2026 06:43 PM

GBP/USD continues to trend lower overall, although the current decline may already be approaching its end. Why do I believe this? First, in my view, the U.S. dollar's recent appreciation has not been fully justified by the fundamental backdrop.

To begin with, the geopolitical conflict in the Middle East has ended, yet it was the primary driver of the dollar's strength throughout 2026. It is therefore somewhat contradictory to see the dollar rise first because of the war and then continue rising after the conflict has effectively ended.

Second, although the FOMC meeting and the Federal Reserve's hawkish stance could certainly have supported the dollar, the rally has become unusually prolonged in recent weeks.

Third, the FOMC has not yet begun its tightening cycle, while the Bank of England could eventually follow the Fed's path.

Fourth, central banks have resumed reducing their U.S. dollar reserves, lowering global demand for the dollar.

Finally, an increasing number of analysts warn that the U.S. stock market may be in bubble territory, with the risk of a sharp correction at any time.

Overall, I believe the bears have already extracted the maximum benefit from the circumstances that developed in 2026.

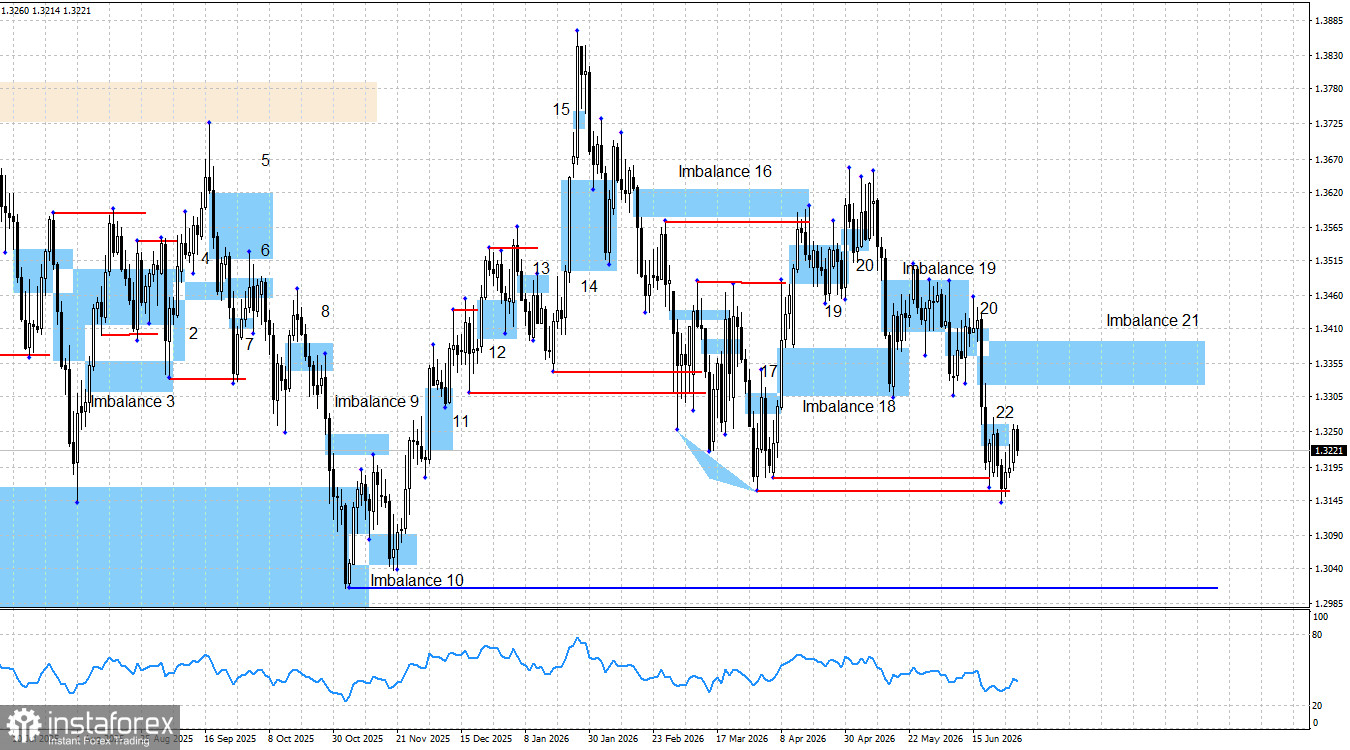

From a technical perspective, however, the chart now allows for at least a recovery toward 1.3322. The market reacted to Bearish Imbalance 22, but the response was relatively weak. Price first swept liquidity below the April 6 low and then below the March 31 low. As a result, we have both a weak reaction to the bearish imbalance and two completed bullish liquidity sweeps. At a minimum, this suggests that a corrective rebound should follow.

Considering that the U.S. dollar still lacks strong fundamental support for a sustained long-term rally and has already posted impressive gains during 2026, I believe the bears may struggle to extend the current decline. Nevertheless, technical analysis should always remain the primary guide. Unless bullish patterns and confirmation signals appear, opening long positions would be premature. Otherwise, traders should wait for the market's reaction to Imbalance 21.

At present, the market remains cautious regarding the agreement between Iran and the United States. However, it can at least be said that the active phase of the conflict has officially ended, at least for now. Although the Federal Reserve triggered a strong rally in the U.S. dollar, it remains unclear what could provide sufficient momentum for bears to continue pressing their advantage. In my view, the broader trend remains bullish despite this year's significant decline in GBP/USD, which has not always been fully supported by fundamentals.

The current technical picture is straightforward. Last week, price reacted to Imbalance 22, but the response was weak, increasing the probability that the current bearish impulse is nearing completion. I would also highlight the liquidity sweeps below the two most recent lows (marked by the red lines), which warn of a possible bullish reversal.

There were no significant economic releases on Tuesday, and traders have shifted their attention to the upcoming U.S. labor market reports, which are traditionally published at the beginning of each month. If this week's Nonfarm Payrolls, unemployment rate, ADP Employment Change, JOLTS Job Openings, and even the ISM Manufacturing PMI once again produce strong results, the bears could renew their offensive. Consequently, market sentiment this week will largely depend on incoming economic data.

Overall, I continue to believe that the long-term fundamental backdrop favors a weaker U.S. dollar. Neither the conflict between Iran and the United States nor the possibility of additional Federal Reserve rate hikes in 2026 has materially changed that view. Geopolitical tensions temporarily reminded investors of the dollar's safe-haven status, but the conflict has either ended or is moving toward a resolution.

The Federal Reserve may raise interest rates again in 2026, which is supportive for the dollar. However, tighter monetary policy also increases the risk of slowing U.S. economic growth. Moreover, Kevin Warsh was appointed as FOMC Chair by Donald Trump with broader objectives than simply maintaining restrictive monetary policy. In my opinion, any additional Fed tightening is unlikely to develop into a prolonged tightening cycle. Therefore, I continue to view any further appreciation of the U.S. dollar as temporary rather than structural.

Economic Calendar (U.S. and United Kingdom)

The economic calendar for July 1 contains three events, all of which can be considered important. As a result, macroeconomic developments are likely to influence market sentiment during the second half of Wednesday's trading session.

GBP/USD Outlook and Trading Recommendations

From a long-term perspective, the outlook for the British pound remains bullish. The reaction to Bearish Imbalance 22 produced only limited selling pressure. Consequently, although a fresh sell signal emerged this week, GBP/USD has been trading largely sideways for nearly a year on the weekly chart, meaning that the current decline can primarily be explained by technical factors. Within a trading range, price movements can develop in either direction.

The pound could still decline toward 1.3007, the level that would invalidate the broader bullish trend, but such a move would require new bearish patterns and confirmation signals. At the same time, the two recent liquidity sweeps favor the bullish scenario. If a bullish Smart Money pattern forms, buyers will have a much stronger technical foundation for a recovery. At present, no new bearish confirmation signals have emerged.